Purpose

The purpose of this procedure is to set out a process for how Complaints should be handled with by Private 3 Money Ltd “P3M”. P3M always endeavours to offer the best possible service to clients and always treat them fairly. In instances where clients feel disappointed, we are required to ensure that complaints are dealt with quickly, impartially and in accordance with the regulations. This policy document should be considered in conjunction with the Privat 3 Money Ltd Treating Customers Fairly and Conduct Risk Policy and procedure.

Objectives

This policy provides employees with a guide to ensuring that upon notification of a dissatisfaction or complaint that business and regulatory requirements are adhered to, and all steps are taken to resolve any issues or problems.

The regime is set out in the PSRs 2017 and EMRs. Most e-money issuers will be carrying on payment services in addition to issuing e-money so will need to be familiar with both the PSRs 2017 and the EMRs.*

Ownership

The Chief Operating Officer “COO” is responsible for the implementation of the Complaints Handling Policy & Procedure.

The COO has overall responsibility for the handling of complaints. However, dissatisfaction is normally raised and discussed with the Relationship Manager in the first instance.

All complaints will be investigated thoroughly.

Complaints will be registered by a member of Senior Management in electronic form and will be reviewed by the COO and forwarded to the Board of Directors on a quarterly basis. In turn, these will be reported to the FCA. (This should be reviewed in conjunction with the Treating Customer Fairly and Conduct Risk policy and procedures).

What is a Complaint?

A Complaint can be made verbally by telephone, in person, or via a written communication delivered in person, via post, e-mail or fax. and This will be a written or verbal expression of dissatisfaction, whether justified or not, from, or on behalf of, a payment service user about the provision of, or failure to provide, a financial service or a redress determination:

(a) which alleges that the complainant has suffered (or may suffer) financial loss, material distress or material inconvenience; and

(b) concerning the rights and obligations arising under Parts 6 and 7 of the Payment Services Regulations.

What is a PSD Complaint?

A PSD complaint is a complaint that relates to the conduct of business rules in the Payment

Services Regulations 2017 (the PSRs). The conduct of business rules fall into two main categories:

- Information that must be provided to customers before and after the execution of a payment transaction (for example, as part of terms and conditions) (Part 6 of the PSRs); and

- The rights and obligations of both the payment service provider and the customer in relation to payment transactions (e.g. charges, consent, liability etc.) (Part 7 of the PSRs).

What is an EMD Complaint?

An EMD complaint is a complaint that relates to the conduct of business rules in the Electronic Money Regulations 2011 (EMRs).

• Part 5 of the EMRs sets out the rights and obligations in relation to the issuance and redemption of e-money.

An eligible complainant is anyone who is eligible to bring a complaint to the Financial Ombudsman Service.

Potential Scenarios

The complaint should be handled in the first Instance by the Relationship Manager responsible for the account, in consultation with the Chief Operating Officer, and resolution of the complaint sought. If the complaint is capable of being resolved the same business day as it is received, any agreed course of action should be taken and a file note made and inserted on the customer’s file, together with any copy correspondence.

If a complaint is not capable of resolution the same business day as it is received, a brief written explanation of the matter of the complaint should be provided by the Relationship Manager responsible for the account, together with any written correspondence from the customer concerned. At this point in time, an entry should be made in the Complaints Register and the date of receipt of the complaint recorded in the Complaints Log.

To ensure that complaints are fairly, consistently, and promptly dealt with, the COO must be consulted, and any proposed course of action or correspondence signed off by him. The COO will be responsible for ensuring that any complaint is properly investigated and that the required timetable set by the FCA rules is adhered to.

If a complaint identifies a systemic, recurring, or specific problem, the COO will advise the Chief Executive Officer of the problem and seek to resolve it via discussion and the implementation of any conclusions arrived at.

All records of complaints will be forwarded to the Risk Committee and will be made available for any necessary reporting to the FCA.

If clients remain dissatisfied and are seeking resolution as a private individual or as a small business, charity or trust with an annual turnover of less than GBP 1 million, they may refer the matter to the Financial Ombudsman Service (FOS) at South Quay Plaza, 183 Marsh Wall, London E14 9SR, call them on

+44 (0) 845 080 1800 or email: enquiries@financial-ombudsman.org.uk

For further information regarding FOS please visit their website www.financial-ombudsman.org.uk

The Second Payment Services Directive (PSD2) sets out requirements for dispute resolution, including response timeframes and complaint reporting requirements.

Complaint Handling Timeframes

When dealing with a PSD/EMD complaint, payment service providers must provide a full written response within 15 business days, or 35 business days in exceptional circumstances. This is to comply with n DISP 1.6.2A.

A final response is a written response from the company which accepts the complaint and, if appropriate, offers redress (appropriate redress may not involve financial redress, it may, for example, simply involve an apology); or offers redress without accepting the complaint or rejects the complaint and gives reasons for doing so, and which informs the customer that, if he remains dissatisfied with the company’s response, he may now refer his complaint to the Financial Ombudsman Service (“FOS”) which, should he wish to do so.

P3M must inform a customer within 15 business days if their complaint is considered to involve exceptional circumstances and indicate the reasons for the delayed response.

Customers have the right to refer their complaint to the Financial Ombudsman Service 35 business days after the payment service provider has received their complaint or after 15 business days where they have not received a holding response.

If we are unable to give a final response within 15 business days (35 business days in exceptional circumstances) we must give a written response that:

- Explains why it is not in a position to make a final response and indicates when it expects to be able to provide one;

- Informs the complainant that he may now refer the complaint to the Financial Ombudsman Service; and

- Encloses a copy of the Financial Ombudsman Service standard explanatory leaflet.

A complaint will be deemed to be closed where the company has sent a final response or where the customer has indicated in writing acceptance of the company’s earlier response.

All staff are required to sign a copy of these internal complaints procedures to confirm that they have received, read, and agree to be bound by the requirements placed upon by them by these procedures as part of their contract of employment and the employee handbook.

FCA Reporting

Privat 3 Money has to complete the Payment Services Complaint Return on an annual basis.

We must ensure we are able to identify and triage PSD2 complaints, including separating out

elements of multifaceted complaints into PSD/EMD and non-PSD/EMD.

Where Can I Find the New Complaint Handling Rules?

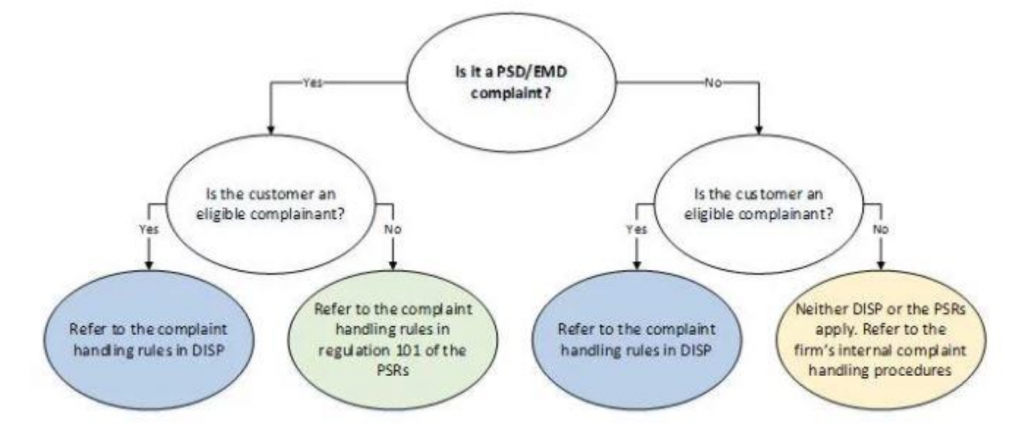

The rules for handling complaints from eligible complainants are set out in DISP (the Dispute Resolution: Complaint’s sourcebook in the FCA handbook). The rules within DISP differ depending on whether the complaint is a PSD/EMD complaint or not.

The rules for handling PSD/EMD complaints from non-eligible complainants are set out in regulation 101 of the PSRs.

The below decision tree helps determine which complaint handling rules apply in which circumstances.

Where a complaint is a non-PSD complaint from a non-eligible complainant, neither DISP nor the PSRs apply. Therefore, there are no regulatory obligations for dealing with the complaint.

Record Keeping

A Central Record of complaints is maintained, where notes and correspondence of all complaints is saved.

Records must be maintained for a minimum of 5 years from the date of receiving the complaint. This must include but it not limited to the following:

- The name of the complainant

- The details of the complaint and any supporting documentation

- The correspondence including the redress

Financial Ombudsman Service (FOS)

If our client is not satisfied with the outcome of their complaint, they can request a review from FOS which has been established to review eligible complaints where firms are unable to resolve.

In the final response to the client P3M will confirm if they are eligible to refer this to FOS.

Contact Details:

Financial Ombudsman Service Exchange Tower,

London,

E14 9SR

Contact Number: 0800 023 4567

Email: complaint.info@financial-ombudsman.org.uk